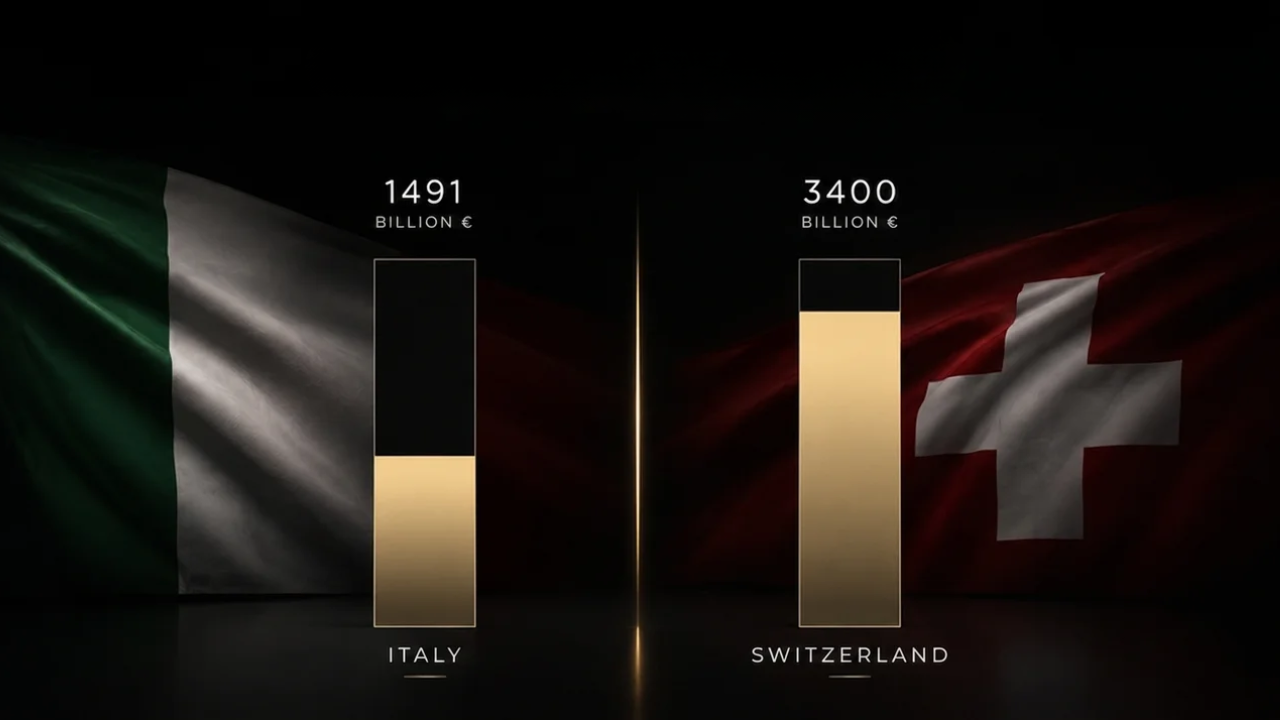

AIPB-Prometeia data published in May 2026 tells a story of structural growth in Italian private banking. Assets managed by Italian private banks will reach €1,491 billion by year end, with a 5.2% increase on 2025 and a share equal to approximately 36% of Italian families’ investable wealth.

These are solid numbers, telling a story of an expanding system sustained by the wealth growth of Italian entrepreneurs and greater awareness of the value of structured wealth management compared to traditional retail deposits.

It’s an important signal, but it’s not enough to define the global reference level of the sector: for service standards, depth of relationship and wealth management tradition, the comparison remains with Switzerland and Singapore.

Switzerland leads: assets managed by Swiss private banks reached 3,400 billion francs already in 2024. Singapore follows closely as the equivalent Asian reference.

For HNWIs evaluating where to allocate the significant portion of their liquid wealth, this difference between domestic market and global industry standards matters concretely.

Italian private banking and the international reference: two different levels

Private banking in Italy is a structured and growing service, but Italian private banks operate in a European regulatory market that, by nature, is less specialized compared to systems historically built around the wealth management of international clientele.

In Switzerland, approximately 90% of significant banking institutions operate under pure private banking regime: structures born to safeguard and grow capital, built with dedicated relationship managers, complete access to global financial markets, and one of the most stable legal and political systems in the world.

Singapore replicates the same model on an Asian scale. Its banking system falls within the “Too Big To Fail” category, regulation is among the most rigorous in the world, and structured multicurrency coverage facilitates the management of international flows in USD, SGD, EUR, GBP and HKD.

For an HNWI with significant liquid wealth, the concrete difference between a domestic private bank and a Swiss or Singapore institution lies not so much in deposit security (domestic banks are also regulated and solid), but in four other points: real geographic diversification of systemic risk, breadth of accessible financial products, depth of the banker relationship, and — a point often left unstated — wealth protection outside the EU regulatory perimeter in case of extraordinary interventions on domestic assets.

What private banking really is

Private banking is a banking and wealth management service designed for clients with liquid wealth starting from hundreds of thousands of euros, who require more personalized and strategic capital management compared to retail banking.

It also means being able to count on a dedicated relationship manager who knows your situation and follows you over time.

It means access to financial instruments reserved for high-level clientele (equities, bonds, ETFs, structured products), operational multicurrency coverage, and an average return on deposited liquidity (usually around 3% annually) that retail deposits don’t reach.

And it means a level of service that makes a difference in the moment you have significant operations to close or problems to resolve.

It’s not a product for everyone.

The realistic minimum threshold to justify the service model is around €500,000-1,000,000 of liquid wealth independently, with access requiring references and complex onboarding processes.

On this point, GloboBanks introduction agreements allow access to private banks (for example in Switzerland and Singapore) with minimum deposits starting from €100,000 — a reduction of up to 90% compared to standard requirements.

If you have significant liquid wealth and are evaluating where to allocate it and in which type of institutions, the first step is a free preliminary analysis of the case with the GloboBanks team: it serves to understand which jurisdiction is realistically compatible with your specific profile before moving any operational step. Schedule it by clicking here.

Switzerland and Singapore: the global reference for private banking

For those asking where to allocate the significant portion of their liquid wealth in 2026, the two reference jurisdictions remain the same as always.

Switzerland is the standard. Political and regulatory stability navigated without disruption through 50 years of financial crises. Structural geopolitical neutrality that other jurisdictions cannot replicate. Complete access to global financial markets and returns on deposited liquidity typically around 3% annually.

Singapore is the equivalent Asian alternative, built to offer the same quality of service in a different Asian regulatory context. For those who explicitly want geographic diversification outside Europe, or have business relationships in the APAC area, it’s the natural choice.

The limit is one: access.

Opening a private account in one of these two jurisdictions independently, without references and without a concrete connection with the country, is a long, costly and often inconclusive process.

Major Swiss banks start from €500,000-1,000,000 minimum deposit for direct applications, require months of due diligence and almost always physical presence for the identification phase. Singapore is practically inaccessible without a verifiable local connection.

.

What changes between direct access and structured introduction

GloboBanks is a banking introduction channel with formal agreements with some of the main Swiss and Singapore private institutions.

Through these agreements, access conditions change substantially compared to the standard published on bank websites.

On minimum deposits.

In Switzerland, the same institutions that require €500,000-1,000,000 initial deposit independently accept introduced clients starting from €100,000-250,000: for the major names of Swiss private banking we’re talking about thresholds reduced up to 90%. In Singapore, an account at one of the main institutions requires a minimum deposit of $200,000 instead of the typical $1-2 million for non-residents without local connection.

On timelines and methods.

Account opening happens entirely remotely in both jurisdictions, without needing to fly to Zurich, Geneva or Singapore for the identification phase. Standard timelines that independently can exceed 4-6 months reduce to 30-60 days on average.

On the banker relationship.

The introduced client enters a relationship that starts from the merit of the profile, not the initial algorithmic screening filter.

On economic conditions.

Wealth management commissions, which standardly are around 1.5%-2% annually, are renegotiated for introduced clients to values around 0.6%-0.8%. On a wealth of €500,000 we’re talking about a difference of €4,500-7,000 per year, every year, for the entire duration of the relationship.

These are the four axes on which a structured introduction channel makes a substantial difference compared to direct application. Everything the bank addresses as standard to the general public (deposits, timelines, physical presence, commissions) becomes negotiable through the channel.

Who it really suits (and who it doesn’t)

Being private institutions, these accounts are not suitable for everyone.

If the available liquid wealth is below €200,000-250,000, the private banking service model is probably not the right choice. The numbers don’t add up on the fee/value ratio, and an accessible-level international premium banking solution does the same job at lower cost.

If the objective is high-volume transactional operability (companies moving millions in recurring commercial payments), private banking is not the right product: private accounts are designed to safeguard capital, not to process daily commercial flows.

If instead the profile is the typical HNWI (high net worth individual), with liquidity between €500,000 and a few million, need for geographic diversification and intention to work with a dedicated banker over the long term, then Switzerland and Singapore remain the natural choice, and structured introduction is the most efficient route to access them.

Want to understand if private banking is the right choice for your profile?

The first step is a free preliminary analysis of the case, by phone, lasting 30-45 minutes, with a senior GloboBanks team consultant. It serves to understand which of the two jurisdictions (or which combination) is realistically compatible with your specific profile, before evaluating which specific institution to open.

From that analysis emerge, with concrete details:

- Which jurisdiction between Switzerland and Singapore is in target for your specific situation

- The realistic minimum deposit for your case through the introduction channel

- The actual commissions you’ll get, item by item, after renegotiation

- The concrete opening timelines for your residency profile

Write at this link to book your preliminary analysis.